1. The Sweet Temptation of Covered Calls: Renting Out Your Stocks

In a volatile market, investors crave consistent cash flow. This is where Covered Calls shine. Think of it as “renting out your stocks as collateral to collect monthly fees.” You agree to give up a portion of your stock’s potential upside in exchange for immediate cash (distributions). It’s a strategy focused on “income now” rather than “growth later.” However, without understanding where this cash comes from, you might be celebrating a gain while your initial investment quietly melts away.

2. Where Does the Cash Come From? The “Return of Capital” Trap

The fuel for covered call distributions is the option premium. You ask another investor, “Want to buy my stock at this price in the future?” and they pay you a fee upfront for that right.

The problem arises when the market is too quiet to generate high premiums, or when the fund earns less than the distribution it promised. To keep investors happy and stay “attractive,” some fund managers sell the underlying stocks to make up the difference.

This is known as “Return of Capital” (ROC) or “Principal Erosion.” While your bank account shows a deposit, your portfolio’s value (NAV) shrinks. Essentially, the fund is giving you back your own money while charging you fees for the privilege.

3. Who in Their Right Mind Buys These Call Options?

Why would someone pay you a fee for the “right to buy” your shares?

- The High-Stakes Leverage Seekers: These traders want massive gains with limited capital. If a stock jumps 50%, a direct investor with $1,000 makes $500. But a call option buyer can control 5,000 shares with that same $1,000 via premiums, potentially netting $25,000 (a 25x return).

- Short Sellers (The Insurance Policy): Institutional players buy call options as “insurance” to cap their losses in case the stock skyrockets.

- Limited Risk: Buyers love that if the stock crashes, they only lose the premium they paid. They’ve limited their downside, and you get paid for taking on that risk.

4. Why Fund Managers Keep “Cutting Into the Bone”

Management fees for Covered Call ETFs are generally much higher than standard ETFs. Fund managers earn their money as a percentage of the total assets you entrust to them.

To attract a large pool of capital, they need a “juicy” yield. Even if option premiums are insufficient, managers are incentivized to maintain high distributions by selling principal. They secure their management fees first, even if it means eroding the fund’s long-term value.

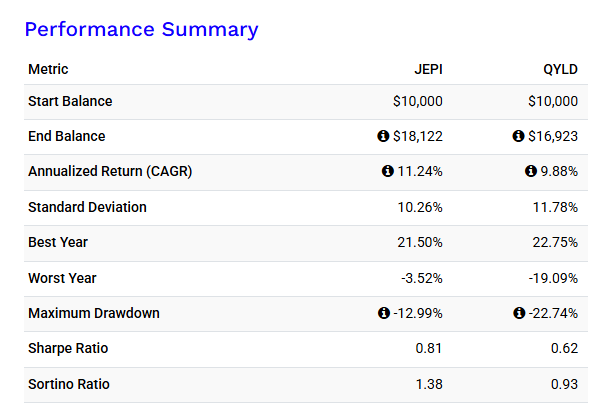

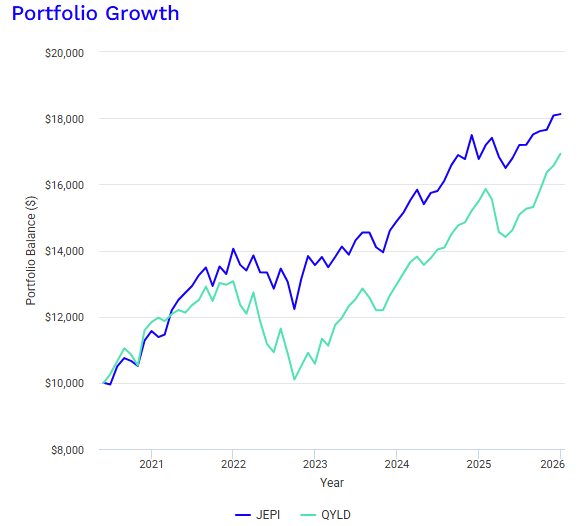

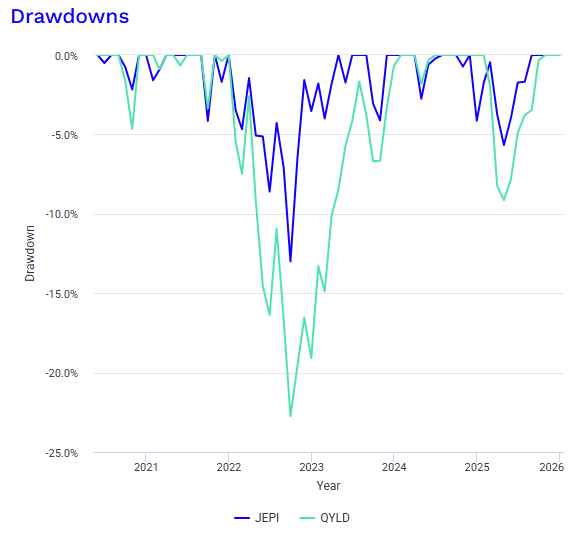

5. Case Study: JEPI vs. QYLD – A Tale of Two Strategies

Comparing JEPI and QYLD reveals the massive difference within the covered call world.

| Feature | JEPI (JPMorgan) | QYLD (Global X) |

| Underlying Asset | S&P 500 (Blue Chip) | NASDAQ 100 (Tech Growth) |

| Option Coverage | Partial (Allows some growth) | 100% (Upside is capped) |

| Income Source | True Dividends + Premiums | Primarily Option Premiums |

JEPI tends to hold its value better in bull markets, while QYLD offers a higher yield by selling away all growth potential. QYLD is a classic example where the long-term chart often trends downward due to high principal erosion.

“Now, let’s take a deep dive into the numbers and conduct a comprehensive performance comparison between JEPI and QYLD from 2020 to 2025.”

6. Dividend Growth Stocks vs. Covered Calls

| Feature | Dividend Growth (e.g., SCHD) | Covered Call (e.g., JEPI) |

| Income Source | Corporate Profits (True Wealth) | Option Premiums (Pre-paid Upside) |

| Bull Market | Excellent. Full Upside | Poor. Gains are Capped |

| Sideways Market | Average. Dividends Only | Excellent. High Premium Income |

7. Final Verdict: 3 Strategic Steps for Successful Income Investing

A Covered Call strategy isn’t a “bad” investment; it’s a tool that requires precise handling. To succeed where others fail, follow these three steps:

- Diversify Your Strategy: Never put 100% of your portfolio into covered calls. Use a 70/30 split between growth stocks and income ETFs to capture market rallies while maintaining a safety net.

- Reinvest Smartly: If you don’t need the cash immediately, reinvest your distributions into “Dividend Growth” assets. This counters the “capped upside” of covered calls by building a secondary engine of capital appreciation.

- Audit Your Yield: Regularly check the fund’s tax documents for “Return of Capital” (ROC) percentages. If the ROC is consistently high during a bull market, your fund is cannibalizing itself to pay you.

Expert Insight: The key to winning is verifying whether the distributions are strictly from option premiums or from your principal. Don’t be blinded by a 12% yield. Look for funds that prioritize “Premium-Only” distributions. True financial freedom comes from choosing honest instruments that protect your principal while fueling your lifestyle.

“Need help choosing between Nasdaq 100 and S&P 500? Click here for the ultimate guide!”